Last 30 Days: Google I/O 2026

Google announced roughly a hundred things in two hours. The betting markets didn't move a point.

About Last 30 Days. Cross-platform research sweeps on topics worth paying attention to. Every post pulls Reddit, X, YouTube, Hacker News, Polymarket, and the web from the last 30 days, then synthesizes what people are actually saying, building, and betting on. Topics get picked when the signal is high and the story is contradictory, when a single headline would lie about the shape of what’s happening. Each post follows the same arc: one specific finding that earns the click, why the topic deserves a sweep right now, the themed synthesis with inline citations, and the follow-up threads worth watching next.

On May 19, Google walked onto the Shoreline stage and shipped what one X recap fairly called “100 things in 2 hours”: a new flagship model, a video world-model, a 24/7 personal agent, an agent-first IDE, agentic Search, smart glasses, a redesigned app, and a price cut on its top tier. The keynote pulled 8.7 million YouTube views in a day.

And then I checked Polymarket. The market for “best AI model at the end of May” still reads Anthropic 96%, Google 1%, OpenAI 1%. Eight-plus million dollars of volume, and Google’s biggest AI day of the year barely registered on it.

That gap is the whole story.

Why this topic deserves a sweep

Most product keynotes can be summed up in a headline. This one can’t, because the announcement volume and the market reaction point in opposite directions, and both are real signals.

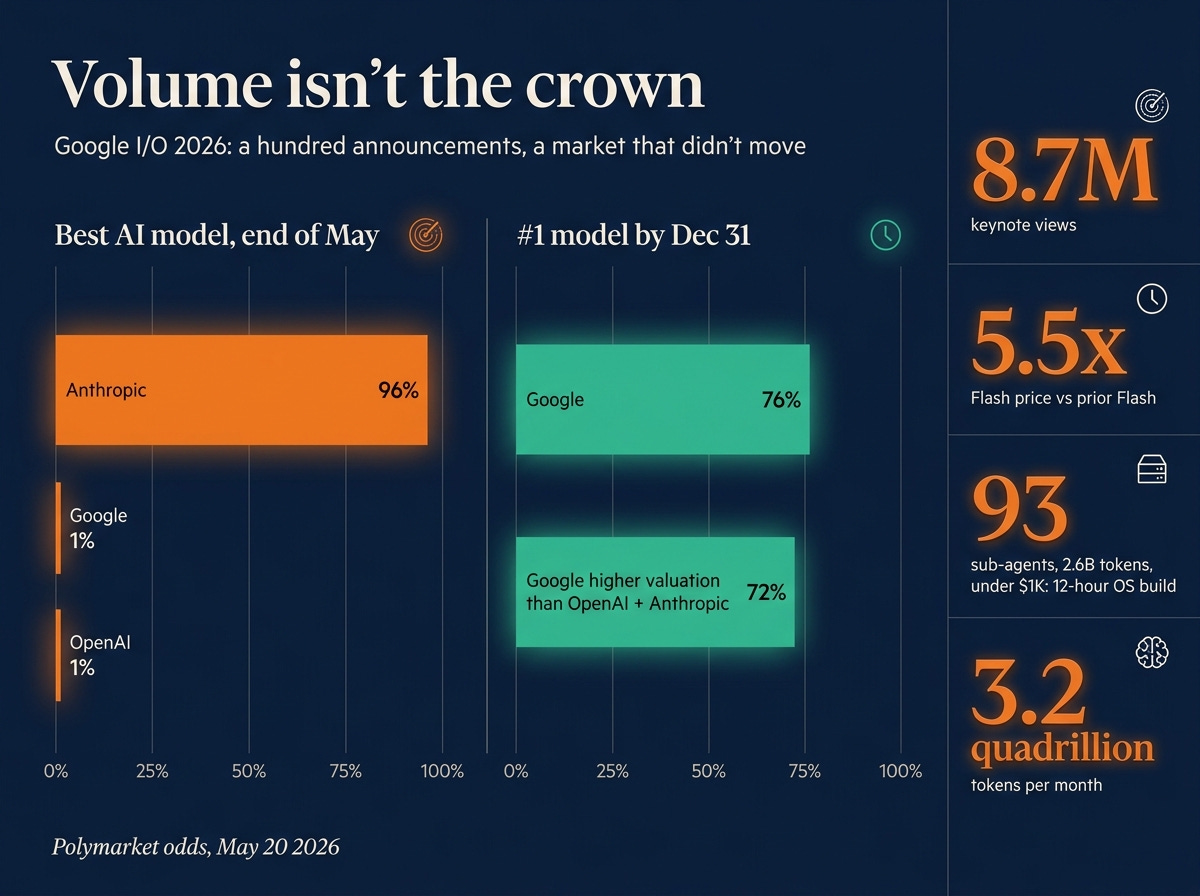

The keynote was, by any literal measure, enormous. Google said it now processes 3.2 quadrillion tokens a month, up sevenfold in a year, and that it expects to spend $180 to $190 billion in capex in 2026, roughly six times the 2022 figure. AI Mode in Search crossed a billion monthly users in twelve months. These are not small numbers, and Google clearly wanted the scale to be the message.

But scale isn’t the same as the crown. The week’s most honest read came not from the launch coverage but from the benchmarks, the pricing, and the prediction markets. Put those next to the keynote reel and you get a far more interesting picture than “Google wins AI.” You get a company that is winning on distribution and time while still trailing on the one question developers actually argue about: whose model is best right now.

So this is a sweep worth running. A single headline would lie about the shape of it.

The model news: fast, capable, and oddly expensive

The centerpiece was Gemini 3.5 Flash, generally available the same day across the app, Search, and the API. Google’s pitch: “frontier intelligence with action.” The headline claim is speed, four times faster output than comparable frontier models, up to twelve times faster inside Google’s own agent harness, with a live demo clocking nearly 1,500 tokens per second writing a playable Chrome dino game. On benchmarks it beats the prior 3.1 Pro across nearly the whole board, with a notable jump on GDPval, the test meant to capture economically valuable real-world work. The heavier 3.5 Pro stayed internal, promised for “next month.”

The branding said Flash. The price tag said something else.

Here’s where it got interesting. According to Artificial Analysis, via latent.space’s recap, 3.5 Flash lands at $1.50 per million input tokens and $9.00 per million output, which they measured as 5.5 times costlier than Gemini 3 Flash and 75% costlier than Gemini 3.1 Pro on their suite. For a tier whose entire identity is “the cheap, fast workhorse you run by default,” that’s a real shift. Developers noticed immediately. The fast-and-capable framing held up. The Flash-means-cheap assumption did not.

The second model is Gemini Omni, a multimodal world-model that takes text, image, audio, or video in and produces editable video out. Google framed it as “the Nano Banana for video moment,” and the live demos (turn a selfie into a black-hole scene, restyle raw footage while preserving the performance) were genuinely strong. The skeptics were not silent. Some called the rougher outputs “B-tier video-game interface” and over-templated. Both things can be true: a clear step up in controllability, not yet a finished product.

The real theme was agents

Strip away the model launches and the spine of the keynote was agents, and on that front Google was more aggressive than I expected.

Antigravity 2.0 is now a standalone, “unabashedly agent-first” desktop app, plus a full CLI, an SDK, and Managed Agents in the API. The harness picked up sub-agents, hooks, and async task management as first-class primitives. The marquee demo was the one everyone’s still talking about:

93 parallel sub-agents, 15,000 model requests, 2.6 billion tokens, twelve hours, under $1,000 in API credits, and out the other end came a functioning operating system built from scratch. Then they played Doom on it, live.

Take the staging with a grain of salt. The point underneath it is architectural, and it’s the same point the pricing makes: Google is betting on many fast, cheap agents running in parallel rather than one expensive monolithic run. The OS demo is a flex, but it’s a coherent flex. It tells you how Google wants you to build.

The consumer-facing version is Gemini Spark, a 24/7 personal agent that runs on dedicated Google Cloud VMs. “Close your laptop,” Google said, and it keeps working in the background, with third-party tools arriving via MCP. Trusted testers got it this week, Ultra subscribers next.

The friction here is sprawl. Developers spent the day asking a fair question: do I use Gemini CLI or Antigravity CLI? Spark or Antigravity? The naming pile (Omni, Spark, Antigravity, Halo, Pix, Flow) is a lot to hold in your head, and a few too many surfaces chasing the same agentic territory.

Search quietly became an agent platform

The change that will touch the most people got the least drama. Google merged AI Mode and AI Overviews into one search experience, live worldwide that day, and wired the Antigravity harness directly into the results page. Ask “how do black holes affect spacetime” and Search now generates a custom interactive visualization on the fly, built per-query. They’re calling it generative UI, it’s free, and it rolls out this summer.

Alongside it: Information Agents that monitor the web 24/7 for whatever you tell them to watch, and a Universal Cart that follows you across Search, YouTube, and Gmail, hunting deals in the background. This is the most consequential bet in the whole keynote, because it changes what a search result is. The model news will be old in three months.

A search box that builds you a tool instead of a list of links is a different thing.

The pricing twist nobody expected

Google cut the price of its top Ultra tier, from $250 a month to $200, and added a new $100 tier with five times the usage limits of Pro. It also moved from daily limits to a compute-credit model that refreshes every five hours.

Cutting the flagship price while raising the workhorse price is a strange pair of moves, and it tells you something. Google wants power users locked into Ultra, and it’s willing to discount to get them. The Flash price hike suggests the economics of “good enough, cheap, at scale” got harder, not easier. Read together, the two changes say Google is repricing around agents that burn tokens by the billion, not around the old chatbot-prompt unit.

The markets didn’t move

Back to where we started, because it’s the cleanest signal in the sweep.

Despite the blitz, the near-term prediction markets stayed put. Best model end of May: Anthropic 96%, Google 1%. The end-of-June market is kinder to Google at roughly 26% against Anthropic’s 70%, but still not a lead. “Gemini 4.0 by June 30” trades at 2% Yes.

And yet the long-horizon markets tell the opposite story. “#1 model by December 31” gives Google 76%. The market on Google’s valuation versus OpenAI and Anthropic combined by year-end puts Google at 72%. So the collective bet is remarkably specific: Google did not take the model crown on I/O day, but it’s the favorite to hold it by year-end, and the heavy favorite to win on distribution and balance sheet regardless.

Volume is not the crown. Distribution and time might be.

That’s the synthesis. The keynote was the most agent-forward thing Google has done, the Search rebuild is the real long-term play, and the money on the table says shipping a hundred things in two hours is a statement of intent, not a change in standings.

What I’m watching next

Does the market drift toward Google as 3.5 Pro ships and developers actually run Flash? The end-of-June Polymarket line is the one to watch. If it doesn’t move off ~26%, the announcements didn’t land where it counts.

The Flash pricing backlash. If “Flash” no longer means cheap, does Google clarify the tiering, or does it cede the default-workhorse slot to a competitor? Watch developer sentiment over the next two weeks.

The 12-hour OS demo, audited. Is “93 sub-agents, 2.6B tokens, under $1K” a repeatable capability or a one-shot showcase? That’s a decode worth doing on its own.

Sources: the Google I/O ’ 26 - (8.7M views) and The Verge’s 35-minute cut; latent.space’s AINews recap (benchmarks + pricing analysis); 9to5Google’s full roundup; CNBC; Tom’s Guide live blog; and Polymarket. Methodology: a last30days cross-platform sweep across Reddit, X, YouTube, Hacker News, Polymarket, and the web, run May 20, 2026, then synthesized.